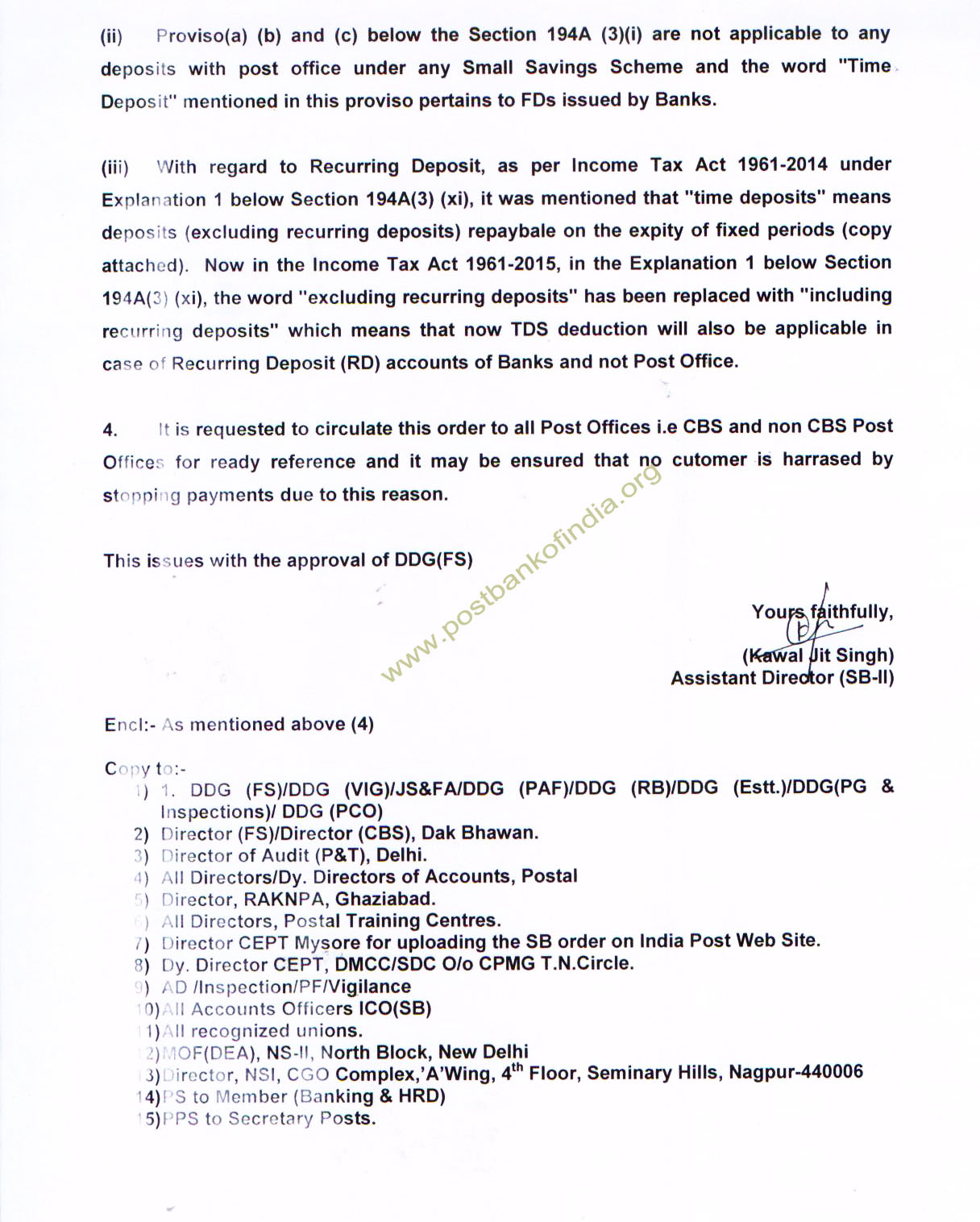

Provision (a) (b) and (c) below the section 194A (3)(i) are not applicable to any deposits with Post Office under any small savings scheme and the word “Time Deposit” mentioned in this provision pertains to FDs issued by Banks.

With regard to Recurring Deposit (RD), as per Income Tax Act 1961-2014 under Explanation 1 below Section 194A(3)(xi), it was mentioned that “Time Deposits” means deposits (excluding recurring deposits) repayable on the expiry of fixed periods. Now in the Income Tax Act 1961-2015, in the Explanation 1 below Section 194A(3)(xi), the word “excluding recurring deposits” has been replaced with “including recurring deposits” which means that now TDS deduction will also be applicable in case of Recurring Deposit (RD) accounts of Banks and not Post Office.

Original SB Order shown below.

Be First to Comment